By James Bamgbose

At a time like this, when public discourse is saturated with claims and counterclaims, the most responsible path forward is to approach the ongoing staff audit controversy in Osun State with objectivity. Allegations bordering financial impropriety and payroll fraud are far too serious to be treated lightly or dismissed on the altar of political affiliations. Yet, even as we interrogate the substance of these claims, it would be intellectually dishonest to ignore the timing of this emergence into the public domain. The manner in which the audit findings were unveiled raises as many questions as the figures contained within them.

Audits are traditionally designed as internal mechanisms for strengthening governance systems and improving fiscal accountability. They are not meant to become media spectacle, but when an audit report claims begins to circulate widely in press briefings before it undergoes institutional scrutiny, it is only natural for suspicion to follow. Was the intent to assist the government in blocking financial leakage or to provoke public outrage before due verification could occur? These are legitimate questions that demand honest answers.

This is particularly also when one considers that the consulting firm at the centre of this controversy is not new to similar engagements across Nigeria. In both Kogi State and Oyo State, the firm previously conducted staff audit exercises that were followed by sweeping disengagements across the civil service. In Kogi State, over ten thousands of workers were dismissed based on findings from a similar audit exercise. Many of those affected insisted they were legitimate employees rather than ghost names on the payroll.

Only a fraction was eventually reinstated after legal review. Fewer than 500 individuals reportedly regained their positions after challenging their dismissal in court. This outcome leaves a troubling gap between the number of those affected and the number able to contest their sackings. It raises the uncomfortable possibility that genuine workers may have lost their jobs without the financial means to challenge the audit findings.

In Oyo State, the aftermath of a comparable audit exercise under the administration of late Sen. Abiola Ajimobi followed a similar trajectory. Thousands of public servants were retrenched after the audit report was submitted to the state government. The backlash from these disengagements triggered significant public resentment against the administration. Over time, this episode became one of the factors cited in discussions about declining public goodwill toward the government in state history.

These historical precedents cannot be dismissed as irrelevant to the current situation in Osun. They raise genuine concerns about the methodological consistency and credibility of the audit firm’s operations. When similar exercises across multiple states produce comparable controversies, it becomes necessary to question the underlying process rather than assume infallibility. Public policy decisions affecting livelihoods must be based on verifiable accuracy rather than speculative conclusions.

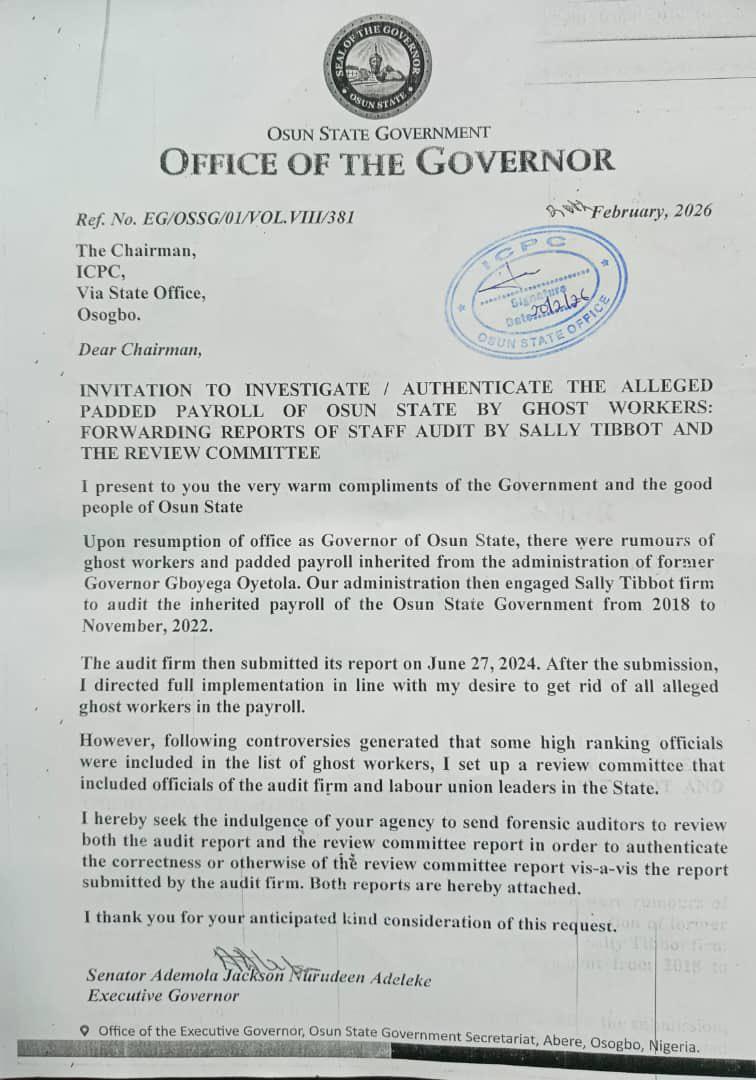

Back in Osun, the situation becomes even more perplexing when one examines the firm’s public conduct during the audit exercise to get the report. In the report, the firm has maintained a firm stance on the alleged ₦13.7 billion in payroll savings identified during the exercise. However, the CEO declined to participate in the review committee constituted by the Osun State Government to validate the audit findings.

Assuming without conceding that the audit report is entirely accurate, why refuse to join a process that would authenticate its conclusions? Participation in an independent review should ordinarily enhance the credibility of any professional audit exercise. Instead, the refusal to engage has created further uncertainty around the report’s integrity. Transparency is best demonstrated through openness to verification rather than resistance to it.

Equally concerning is the apparent inconsistency in the firm’s public statements regarding the number of ghost workers identified from over 8,400 workers in her report in January to 15,000 workers in her recent interview. While the CEO has repeatedly emphasised the ₦13.7 billion figure with remarkable certainty, there appears to be less precision when discussing the total number of affected staff. Financial accuracy must be matched by human accuracy in any credible audit process. Otherwise, the exercise risks devolving into reputational damage rather than systemic reform.

The recent testimonies from within the state’s tertiary education sector have further complicated the narrative. The Vice Chancellor of Osun State University, alongside 249 members of staff, has publicly stated that they were erroneously listed as ghost workers in the audit report. These are individuals whose employment status can be easily verified through institutional records. Their inclusion on such a list raises significant doubts about the reliability of the audit methodology.

Such a development can not simply be dismissed as a minor technical oversight. The wrongful classification of verifiable public servants undermines the credibility of the entire exercise. It also fuels suspicion that the audit process may have prioritised projected savings over factual accuracy. Public confidence in governance systems depends heavily on the perceived integrity of reform initiatives.

This brings us to another critical issue that deserves scrutiny. Reports from the letter of engagement indicate that the firm is to get a percentage share of the identified savings. This financial incentive structure inevitably raises questions about possible conflicts of interest. Was the firm motivated primarily by the desire to enhance payroll transparency through its media calls or by the opportunity to secure its expected close to ₦2 billion share?

It is also instructive that shortly after the firm’s first media appearance in January, Governor Ademola Adeleke formally petitioned the Independent Corrupt Practices Commission to investigate the allegations contained in the audit report to show willingness by the state government to subject itself to external scrutiny. This is not an action to expect from an administration attempting to conceal financial irregularities.

The integrity of any audit exercise lies not only in its conclusions but in the transparency of its verification process. Public policy decisions affecting thousands of livelihoods must be grounded in demonstrable accuracy. If the firm remains confident in its findings, then defending them within an institutional review framework should not have been perceived as an imposition.

In the end, this can not be settled by press statements or headline figures but by a transparent process that stands up to independent scrutiny. Until every question is answered openly by the auditing firm, it remains less a triumph of accountability and more a test of credibility for the consulting firm.

- James Bamgbose writes from Igbajo, Boluwaduro Local Government, and can be reached via email on bamgbosejames9@gmail.com